With business sentiment softening and the property market coming off the boil in Auckland, I thought I would join the bandwagon and talk about the doom and gloom that is prevailing in property investment circles.

As a starting point, I would note the downturn is not unexpected and has been well predicted by many investors, including the writer. In fact, I wrote in my book

Property 101 (published in 2015) that with property cycles peaking on a '7' year, 2018 should be the year things start to slump. After all, this has been the pattern for the last 40 years, with markets peaking in 1987, 1997, 2007, and now 2017. I wonder when the next peak might be?! I don't think you need to be a mathematician to spot the trend: 2027 is my prediction and we have at least 5-6 years of the Auckland market flatlining until we can see upside growth.

I say 5-6 years because it will take at least this amount of time for rents and household incomes to rise, to make asset values start to make sense and allow more growth. Until then, a lack of affordability and cash yield will undermine growth in my view. But then there are many other disruptive factors to consider that affect property values, including interest rates, immigration, housing supply and the Auckland Unitary Plan releasing an estimated 300,000+ consentable dwellings in Auckland (including theoretical airspace and sections). The availability of credit for investors and developers is also topical, with banks becoming predictably bearish in appetite for lending into an increasingly squeamish housing market.

Supply increase biggest concern for Auckland property

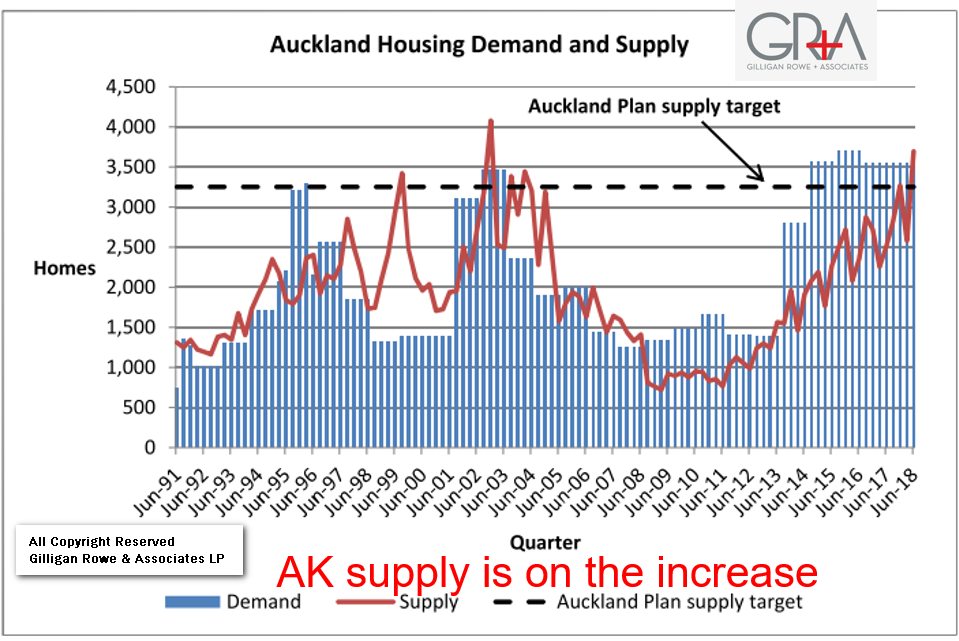

My biggest concern is the rapidly expanding supply of housing in Auckland. With the Unitary Plan becoming successful and quickly increasing supply, I'll let the graph below speak for itself (quarterly household formation in blue and dwelling consents in red). At GRA we crunch this data quarterly for all regions across the country as part of our internal tracking of the New Zealand property market.

John Key predicts economic downturn

John Key predicts economic downturn In a very good recent radio

interview on Newstalk ZB, Sir John Key expressed concerns that we are heading into a global economic downturn), which will naturally impact upon New Zealand.

Some of his reasons include:

•

The growth in US economy being driven by a large budget deficit. Although the US doesn't have a problem today, it has inflated its national debt to in excess of 20 trillion dollars, and therefore it is very likely the US will have a big problem in the future when it tries to unwind this position.

•

There has been an increase in private sector debt in Australia (and to a lesser extent, New Zealand) and there are now more delinquencies, e.g. with property investors not making loan payments on their rental properties.

•

In China there have been a number of corporate collapses, and the Chinese government is reining in credit growth as a result.

According to Key, the question is not if a downturn will occur, but when. Many predict that 'GFC 2' could result.

Key went on to say that although New Zealand came through the 2007-2008 GFC very well (compared to a lot of countries), we are not immune to a downturn in the economy. Many of the factors that have driven our strong growth are affected by changes to government policy. This is causing adverse business conditions and sentiment is rapidly falling. Cited concerns from Key included reducing immigration, a cooling housing market, soft business confidence, and reduced prospects for foreign investment (especially from China). If the New Zealand economy is to continue to grow, these factors will need to be replaced with something else to provide equivalent stimulus, says Key.

On the plus side, New Zealand does not carry a lot of national debt, so we are in a better position than many other countries. Having said that, we are very indebted in terms of our private household debt, with NZ residential mortgage indebtedness being among the highest in the developed world. This would make New Zealand households particularly vulnerable to spikes in inter-bank lending rates, as we will import the cost of credit if disruptive events offshore eventuate. It is for this reason that the writer has favoured longer-term fixed interest rates, over cheaper shorter-term rates. I always say to clients that I consider surviving the ups and downs to be more important than getting the lowest interest rate.

What does this mean for you? The domestic outlook in New Zealand could be affected by disruptive events offshore, as yet undefined but increasingly looking riskier. Trumpian trade wars, European banking default, Chinese government spending changes, geo-political disagreements – all of these things look volatile at present.

If you have debt (e.g. on your home, investment property or a business), assess your capacity to service your loans if interest rates were to spike in the next few years.

o Consider fixing your interest rates long while rates are still low, and have your loans maturing at different times (or divide your borrowing into tranches). You won't get the cheapest rate in the market by doing this, but you will de-risk your household in that you won't have all your debt maturing at the same time when interest rates could be at an all-time high. Further you reduce your exposure to spikes in rates.

o Get lines of credit in place now while you don't need them – such a facility could enable you make your interest payments for a few years should you need to refinance when rates are high.

o One more technical point: we have noted banks being less agreeable to allowing borrowers to roll their interest-only loans back onto interest-only, a trend coming from Australia. If a bank forces you to hold the term of your loan to your original application, this can cause surprisingly difficult cashflow obligations, depending on the term of the original loan.

I recently spoke to Kris Pedersen from

Kris Pedersen Mortgages, and he highlighted this as a risk in the current environment.

o

For example, if you have a loan that is a 20-year term, with 5 years interest-only, then at Year 6 you have to pay the entire principal off over the residual term of 15 years.

o

Compare this to the same loan written on a 30-year term. At Year 6 you can pay the residual off over 25 years principal and interest – much softer cashflow.

o

While we all assume that the banks will cooperate and allow us to re-write interest-only when you end the current term, you have to meet cashflow servicing criteria to do this on the roll-off period. If you can't do this, the bank will hold you to the original loan term and force you on to principal and interest

over the residual term of the loan.

o

Therefore, we recommend looking at your loan terms now, and re-writing them on longer terms to make the roll-off at Year 6 easier, in the event the bank does not allow you to revert back to interest-only.

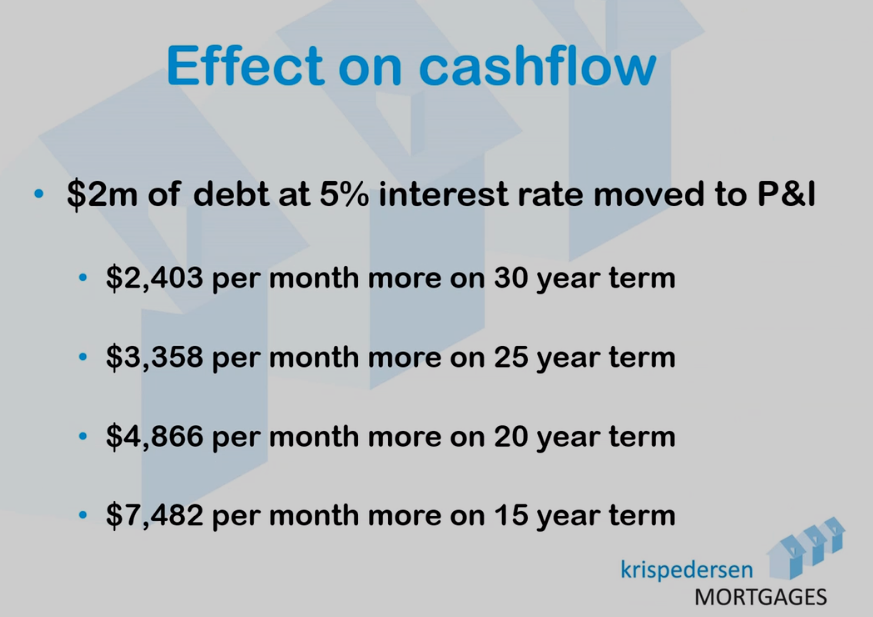

Example cashflow implication of different residual terms, $2m borrowed  Commercial strategies to manage property investor cashflow

Commercial strategies to manage property investor cashflow •

Property investors would be wise to assess their portfolios and consider adopting strategies to increase cashflow (e.g. flat conversions, rent-by-the-room, extra bedrooms from existing dwellings, etc.).

•

If you believe your cashflow could not withstand a spike in rates, we would well recommend selling now to get your house in order. Don't wait for your banker to push you to do it in the worst part of a recessionary downturn.

•

In our experience as a practice, during the downturn investors go broke because of a lack of cashflow (i.e. not being able to service their loans) rather than because property values are decreasing for a time. So consider these recommendations.

•

If buying, ensure you purchase at a discount so you can absorb a decrease in market value without losing equity. In the absence of capital growth prospects, you need to be making money as you buy property at present. Instant equity strategies are key.

•

Ensure you have the right tax and legal structures in place so that your personal assets are protected should something happen with your property investments. If you would like a review of your current structure, talk to your GRA Client Services Manager, or contact us on (09) 522 7955,

[email protected] or

via our online form.

•

Find out what property investment strategies are working at this stage in the cycle – a good education can help prevent you from making costly mistakes. To that end, we invite you to attend one of our

free Property Investment and Education seminars (held online, either by live Zoom or on demand) where you will hear about the strategies are working in this market.

For investors with good cashflow and who, after assessment of the risks, are seemingly immune, we carry on the thankless task of managing our inventory property and watching as the government makes it increasingly challenging with regulation and taxation. Naturally, past performance does not guarantee future performance, but if we continue to get the long-term growth rates Auckland (and much of the the rest of New Zealand) has enjoyed, then we will be well paid for our efforts in 2027, if the past pattern continues.