Otara vs Remuera Case Study

2537POSTED:

Articles by Matthew Gilligan.

Case study

Remuera vs Otara

The Great Property Debate: Cash flow vs Capital Growth

Property investor compares investment returns

Tyson is a property investor, looking at investing in the Auckland market. He has been told by his parents that he should 'buy the worst house in the best area, and only invest where he would be comfortable with having his tenants over to dinner'. (I note that some people call Tyson's parents awful snobs and say they should get out in public a bit more often.) But personal bias and snobbery aside, do Tyson's parents make a valid point? Does the quality of an area and socio-economic status of the tenants dictate returns in the Auckland market?

Tyson decided to test the theory and look at the maths of the 10-year return on two specific suburbs, and make his investing decisions based on numbers, not old sayings and emotion.

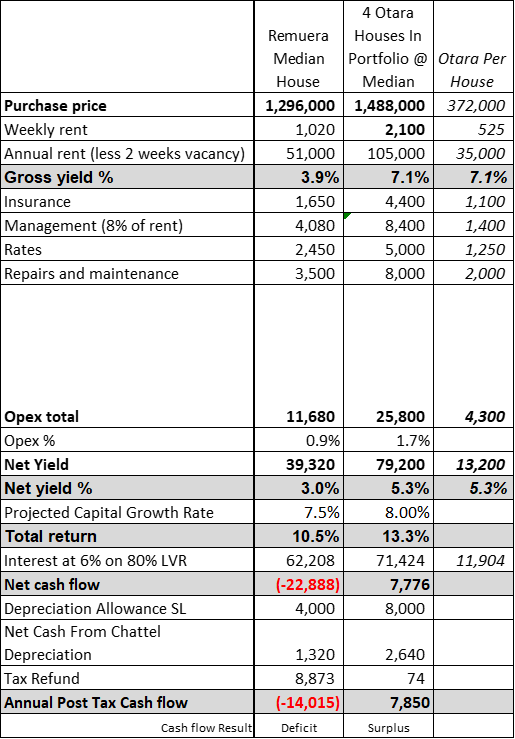

Otara vs Remuera

Tyson was interested that Otara, with its higher cash flow but similar capital growth, won the contest on total return. He wanted further convincing so looked at the five-year and two-year comparative growth rates to see if the shorter term trends were changing. This revealed as follows:

22-year: Otara was doing 22% vs Remuera 17%

9-year: Otara was doing 9.4% vs Remuera 9.3%

5-year: Otara was doing 12.2% vs Remuera 10.5%

2-year: Otara was doing 22.3% vs Remuera 12.5%

Source Property Ventures Real Estate / REINZ Median House Price Data

Otara is still standing up.

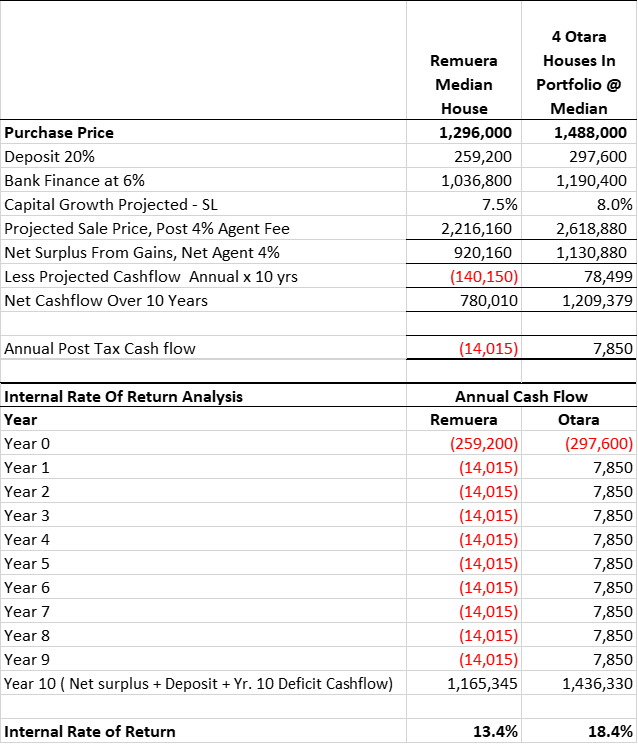

From an internal rate of return (IRR) perspective, selling at year 10, this is how it stacks up:

Comprehensively then, looking at the total return and IRR, Otara keeps up with Remuera's capital growth, but thrashes it when cash yield is added into the analysis.

Author notes & morals of the story

Summary

I am not saying, 'Here is a silver bullet, go buy in South Auckland for cash flow and high growth and this should be your only property strategy'. Far from it. I'm simply pointing out to those that 'want to be able to have their tenants to dinner', that there are other places you can invest in Auckland, and do very well, possibly even better than in the perceived prime residential suburbs.

If you'd like to learn more about property investment strategies, you might be interested in attending one of our upcoming events.

Just wanted to pass on how incredibly impressed I was with Quade Fraser, I have some complicated aspects to my personal situation and was looking at the a purchase of a property while needing to consider multiple individuals, a company and with my contracting and GST considerations.

I asked the consultant multiple questions over our meeting and he was able to calmly and articulately answer everything and give me cause to think about a whole lot of areas I would not have even thought of including; bright line, GST, mixed-use assets, trust structures (considering children beneficiaries), utilising a company structure etc. The bottom line is, I have a much better idea on what we need to do to structure my affairs in the most beneficial way for my family over the long-term.

Very knowledgeable, professional and with a great manner too. I got a huge amount of value out of the meeting.

- Kate, June 2023

Gilligan Rowe and Associates is a chartered accounting firm specialising in property, asset planning, legal structures, taxation and compliance.

We help new, small and medium property investors become long-term successful investors through our education programmes and property portfolio planning advice. With our deep knowledge and experience, we have assisted hundreds of clients build wealth through property investment.

Learn More