Navigating NZ's New FIF Rules

6252POSTED:

Articles by Quade Fraser.

If you're a new migrant to New Zealand, a Kiwi returning home after a long time away, or someone who pays tax in two countries, you've likely encountered New Zealand's complex Foreign Investment Fund (FIF) rules. These rules are designed to tax New Zealand residents on their offshore equity / share investments on a realised and also often an unrealised basis.

Historically, the FIF regime has created challenges for taxpayers, particularly due to the cashflow impact of tax liabilities arising without any corresponding income / cash, as well as the potential for double taxation. To address this, a new calculation method has been introduced to try and align tax with the realisation of cash from your FIF investments: the Revenue Account Method, or RAM.

This guide will walk you through what RAM is, who it's designed for, and when it might (or might not) be the right choice for you.

Important note: At the time of writing this article, there is a proposal to extend these rules to all New Zealand tax residents. (This was included in the 2026 Budget.) Draft legislation is expected in August/September 2026, and we will provide an update as soon as we have confirmation that the rules will change.

Key Takeaways

In simple terms, RAM changes when and how you pay tax on certain foreign share investments. Instead of taxing you each year on a "deemed" return (an assumed profit), RAM generally taxes you on a realisation basis. This means tax is typically payable only when:

1. You receive a dividend from your investment

2. You sell your investment and make a gain

3. Your investment stops being eligible for RAM (for example, if an unlisted company lists on a stock exchange, which would trigger a deemed sale for tax purposes).

A key feature of RAM is that any gain you make on the sale of a qualifying investment is discounted by 30% before tax is applied. This means you only include 70% of the gain as taxable income, which is then taxed at your marginal rate. Dividends, however, are fully taxable.

It is important to note that there are two applications of the RAM method:

1. Ordinary – for new migrants and returning Kiwis with eligible unlisted shares.

2. Extended – which applies to individuals who are taxed on their FIFs in two (or more) countries based on their citizenship or right to reside, and that country has a double tax agreement with NZ.

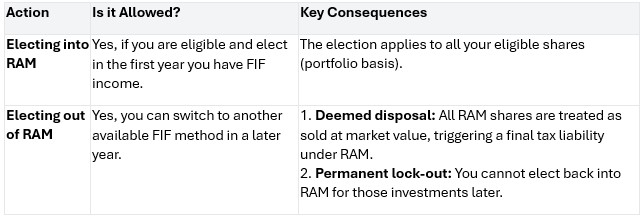

The RAM is designed to be elective, which includes the ability to elect out of the method in a later year and switch to another available FIF calculation method, such as the Cost Method or Fair Dividend Rate (FDR) method.

You cannot apply RAM for an investment once another method has been applied.

The election to use RAM applies on a portfolio basis to all of your eligible shares. If you decide to stop using RAM, this decision will also apply to your entire RAM portfolio and can have significant implications, as outlined below:

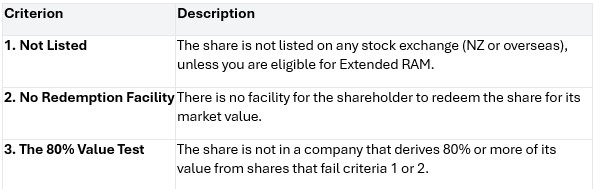

An "eligible unlisted share" is a share in a foreign company that qualifies as a RAM interest. For a new migrant or returning New Zealander, the share must not only meet the criteria below but must also have been acquired before they became a New Zealand tax resident.

There are three key characteristics a share must have to be eligible:

RAM is not for everyone. It's a targeted solution for specific groups who have been disadvantaged by the existing FIF rules.

RAM does not apply to companies; its application is limited to natural persons or trusts.

1. New Migrants and Returning New Zealanders

1. If you became a New Zealand tax resident on or after 1 April 2024 following at least five years of non-residency; or

2. You were a tax resident before 1 April 2024 but qualified for transitional residency that ceased after 1 April 2024; and

i. you have shares in an unlisted company; and

ii. you acquired those shares before becoming a NZ tax resident (or had the right to acquire)

you may be eligible to use RAM.

Previously, the FIF rules could force you to get expensive and difficult valuations for these unlisted shares every year or force you to pay tax on 5% of the cost of your FIFs each year (with deemed appreciation at 5% annually). RAM solves this by taxing the gain only on specific realisation events (e.g. when the company lists or when you sell the shares).

Example 1A: The New Migrant

Anja moved to New Zealand and became a tax resident on 1 June 2025. Before moving, she owned shares in an unlisted European tech company, which she bought for $50,000.

At the time of triggering NZ tax residency on 1 June 2025, an independent valuation of the shares determines they were worth $200,000. This becomes her "cost base" for NZ tax purposes.

In 2028, Anja sells the shares for $220,000. Anja’s tax rate is 39%

Let’s look at Anja’s tax liabilities using the RAM and Cost methods to see how they compare.

Tax calculation under RAM

• Capital Gain: $220,000 (sale price) - $200,000 (cost base) = $20,000

• Taxable Gain (70% of total): $20,000 x 70% = $14,000

• Tax to Pay: $14,000 x 39% = $5,460

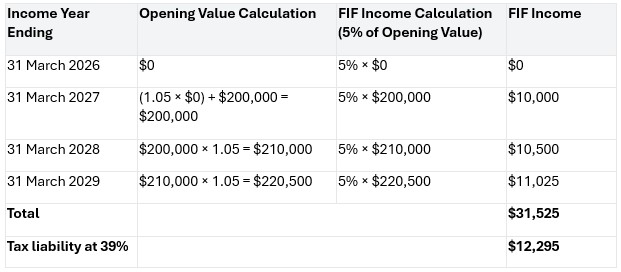

Tax calculation under Cost FIF method (5% of opening value adjusted annually)

Comparison

So in this case, RAM results in a much more favourable outcome for Anja. In other words, if the capital growth following tax residency is not significant, RAM can result in a better tax outcome than using the Cost Method (though naturally, you are holding the stock because you expect greater returns).

Now let’s look at the same scenario, but with a much larger capital gain.

Example 1B: Same example but sale price is $500k

Tax calculation under RAM

• Capital Gain: $500,000 (sale price) - $200,000 (cost base) = $300,000

• Taxable Gain (70% of total): $300,000 x 70% = $210,000

• Tax to Pay: $210,000 x 39% = $81,900

Tax calculation under Cost Method

This is the same as for the previous example.

• Total Taxable FIF Income: $31,525

• Tax to pay: $31,525 × 39% = $12,295

Comparison

As you can see, the RAM method isn’t always sunshine and rainbows. If you expect the stock to increase significantly after becoming a NZ tax resident, you will be better off applying the Cost Method, as illustrated above.

2. Dual Tax Residents (Extended RAM)

Many individuals have tax obligations in more than one country. This is common for US citizens and Green Card holders living in New Zealand, as the US taxes them on their worldwide income regardless of where they live. This creates a risk of double taxation, as NZ's FIF rules could tax unrealised gains annually, while the US only taxes gains upon sale.

To solve this timing mismatch, an "Extended RAM" is available. If you are liable to tax in another country (that has a tax treaty with NZ) based on your citizenship or right to reside, you may be able to use RAM for a wider range of investments, including listed shares.

Example 2: The US Green Card Holder

David is a US Green Card holder and a NZ tax resident. He buys $100,000 worth of listed shares in a US company.

Because the NZ tax is triggered at the same time as the US tax (on the sale), David can now use foreign tax credits to offset his NZ tax liability to ensure he doesn't pay tax twice on the same gain.

A significant feature of the RAM rules relates to when you cease to be a New Zealand tax resident. This is often referred to as a "deferred realisation tax" or "exit tax".

When you leave NZ, you are treated as having sold all your RAM investments at their market value on the day before you become a non-resident. This creates a "deemed disposal" and a potential tax liability.

However, there is an important condition: this deemed disposal is only taxed if you sell the actual investment within three years of leaving New Zealand.

If you hold onto the investment and sell it more than three years after you have left NZ (and you haven't returned to become a resident again in that time), the original deemed disposal is disregarded. Because you are a non-resident at the time of the actual sale, there is no New Zealand tax to pay on that gain.

Using our earlier example, if Anja left NZ on 1 July 2029 and sold her shares on 1 August 2032 (more than three years later), she would pay no NZ FIF tax on the sale.

As shown in the examples above, RAM is not always the best option. For investments with very high growth potential, the Cost Method may result in a much lower tax bill. The decision to use RAM is an important one and requires consideration of wider factors such as expected growth, future place of residence, and timing of expected sale.

The Cost Method is an alternative for investments where the market value is not readily available. Under this method, your FIF income is typically calculated as 5% of the investment's "opening value", which starts at its original cost and increases by 5% each subsequent year.

Summary

The introduction of RAM is a positive step towards a fairer and more practical FIF regime for certain taxpayers. However, its targeted nature means that careful, individualised assessment is essential. This makes it imperative to seek professional tax advice before adopting any FIF method – contact us at GRA if you’d like help with this.

Hi Salesh, I just wanted to send you an email on behalf of GRA to say how fantastic we have found your company to date. As you know, Ben and I joined GRA a couple of months ago and have just found you so amazingly helpful in getting our new property set up correctly and sorted out. We have what I would consider a rather complicated structure as a result and it’s a fantastic feeling to know that we are getting everything done in the best way possible. We have just had approval to put a minor dwelling on the property which will make a massive difference in terms of cash flow and obviously value, something we would never have even thought of without GRA and which we are very excited about. During the buying process we attended a seminar with Matthew and from the outset thought he was fab. We therein signed up for property school and found this nothing short of fantastic. The content was relevant, up to date and comprehensive, but more importantly it was taught in a way that we could actually understand and really get value out of. I wanted to mention also, that everybody GRA have recommended to us has been just so efficient and absolute masters at what they do. A wonderful network of people that we feel very lucky to now be able to call on. From Kris Pederson and Bryan Rist who put our mortgage together to the insurance guys they then referred us to, I’m super impressed. Within GRA, Ellery has probably turned things around for us faster than I’ve ever known before, something which we appreciated so very much when it came to crunch time. She’s always a pleasure to deal with and again, we’re stoked. We’ve just settled on the property today and are about to go and get the keys. I’m pretty pumped and hence this email is probably rather excitable. So, a massive thank you to you Salesh, the partners for such a fabulous 6 weeks at property school and everyone at GRA for their help. May this be the start of our property empire. Thanks again, - A & B - July 2015

Investing in residential property?

If you're investing in residential property, seeking to maximise your ability to succeed and minimise risk, then this is a 'must read'.

Matthew Gilligan provides a fresh look at residential property investment from an experienced investor’s viewpoint. Written in easy to understand language and including many case studies, Matthew explains the ins and outs of successful property investment.