The

RBNZ has told banks that they must adopt ‘sensible lending’ practices, which means they need to stress test their clients’ ability to make their loan repayments. What do we mean by stress test? They are now testing investors on 8% principal and interest over 25 years, and reducing the rental income they’ll take into account by 25–30%.

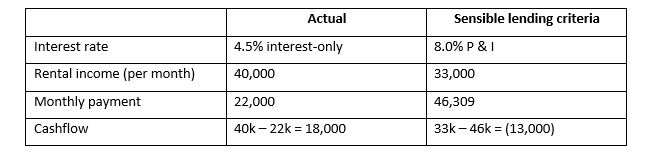

Bearing in mind that current interest rates are around 4.5%, and many investors will take out interest-only loans, these new criteria can very quickly make a cashflow positive investor look like their cashflow is negative. Result? The bank won’t approve finance. I’ll illustrate with an example.

Suzanna has built a good portfolio of properties and has $6 million of debt. Her current repayments are in the ‘Actual’ column of the table below. If she were to approach the bank today, they would assess her as per the ‘Sensible lending criteria’ column.

Based on today’s reality, Suzanna has $18,000 positive cashflow, so can easily service her loans. However, using the bank’s criteria, she is backwards by $13,000, which means she fails the bank’s serviceability test and they will not lend her anything.

Even if we look at the situation when Suzanna comes off interest-only onto P & I at today’s rates, meaning her monthly payments increase to $30k, she is still ahead by $10,000.

How can investors manage in this ‘sensible lending’ environment? There are a number of things

property investors can do to be able to continue investing under these stricter rules, including:

- Arrange lines of credit with your bank now, before you need them.

- Reduce your credit card limits before applying for finance – even if you only ever use a fraction of your credit card limit and you pay your entire balance off each and every month, the banks look at the credit you have available and assume you will use all of it when they assess you. You can increase your limits later if you need to.

- Don’t apply for a new credit card until you have your lending in place.

- Make friends with your banker – if they know you and you treat them well, they will be inclined to do what they can to help you. For example, buy them a Christmas gift, take them out for coffee occasionally.

- To meet the new bank servicing requirements, many investors will need a bigger deposit, so you may want to consider working with a JV (joint venture) partner. Lots of our clients do this, and as long as you have a robust shareholders’ agreement, JVs can work very well.

There are good opportunities to be had in the cooling property market. To be able to take advantage of them, you need to be aware of the new lending serviceability criteria and put things in place so you can qualify for finance. In this regard, it pays to talk to a good mortgage broker – I personally recommend Kris Pedersen from Kris Pedersen Mortgages, who you can

contact here.

Additionally, it is advisable to ensure your borrowing is

structured correctly from tax efficiency and asset protection perspectives, and this is something we can help you with at GRA. You can contact us on (09) 522 7955,

[email protected] or

via our website.