Renting versus owning: Is home ownership bad business?

2539POSTED:

Articles by Matthew Gilligan.

In 2012, the media focused on the comments of an economist, Shamubeel Eaqub, who is well documented for being anti-property. Bear in mind the media likes to present two sides to a story, in this case the counter point in the property debate. So Mr Eaqub fits the ticket for anything related to property bashing.

Of note was this economist's claim that owning property as a family home in New Zealand does not make sense, that you are better to rent houses and invest your home equity in the stock exchange. I found this information counter intuitive in relation to the property I routinely get involved with, so crunched the numbers.

To be fair, in a 2014 reader poll (by The Visible Hand in Economics), Mr Eaqub was voted the fourth sexiest economist in New Zealand – I take my hat off to him. However, I don't think he will ever be the richest economist, based on his statement that the ownership of houses is bad business. He called buying a house a 'loss-making business' and recommended that people invest their money in the share market instead. I have many self-made multi-millionaires as clients who made their money in buying residential property. In fact one of my staff members just made his second million (in equity), buying houses in Auckland. He just turned 30. I don't think owning your own home or rental investments is a bad business, but let's take a closer look.

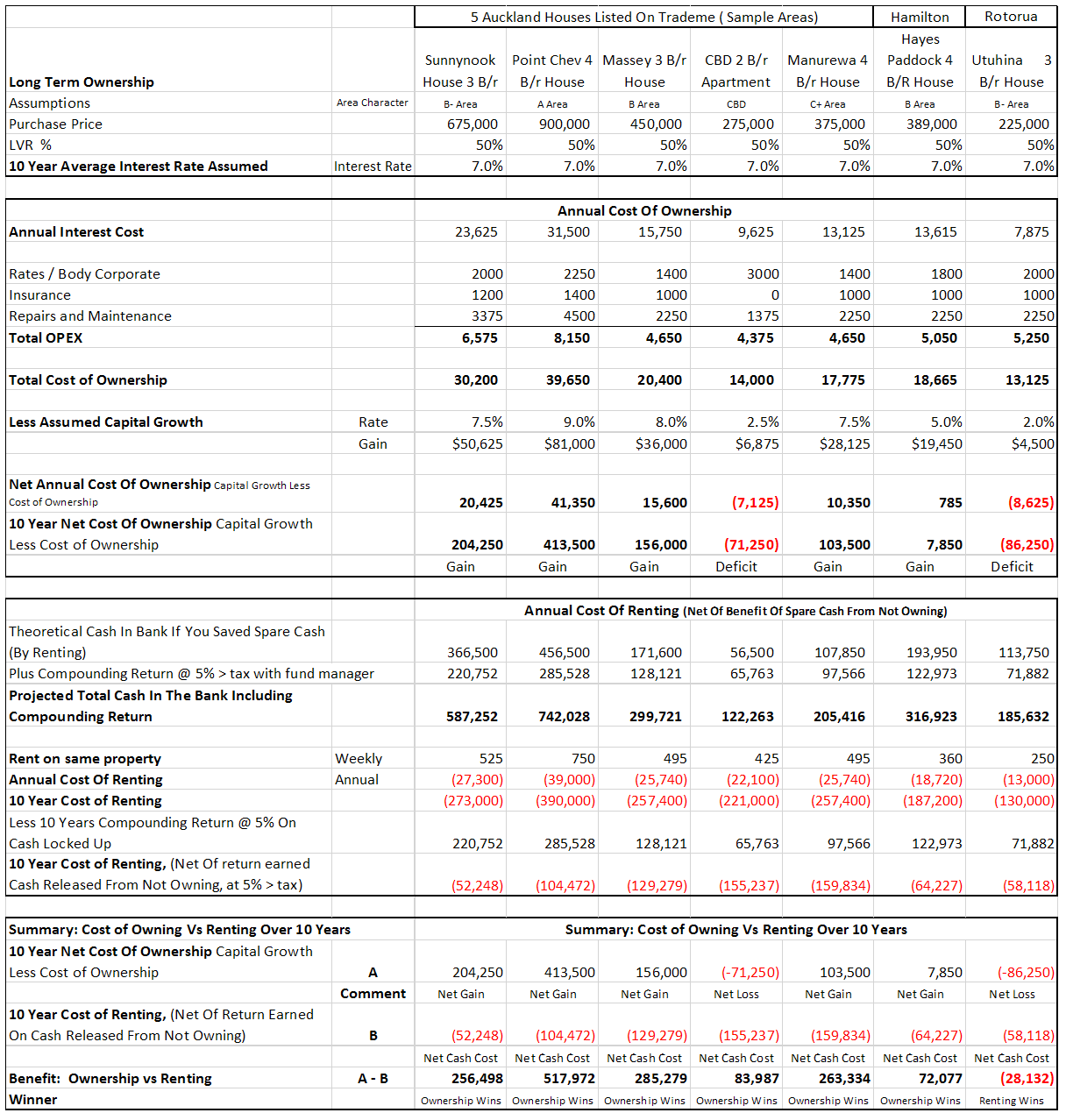

I did the maths on five houses in Auckland and a few down country. The table below shows what they look like with 50% finance and capital growth rates that are representative of the areas these properties are in, versus renting them. I calculate where you are if you own the houses and get capital growth, versus using the extra cash you would have if you rented and invested the surplus (including the starting equity from selling the house) into shares at a 5% after tax return.

I know people may raise their eyebrows over my capital growth rate assumptions at 7.5%–9% for Auckland houses, but let's face it, Auckland has a land supply problem. It is not solved in the short to medium term by the Auckland Unitary Plan, as there are significant lead times to getting the services in the ground and the rules in place to bring land supply on tap. I acknowledge that projected growth rates are subjective and affect the above analysis, but further note that if you change the capital growth rates to say 6%, ownership still wins.

A few more points of contention are:

To explain the analysis (if the spreadsheet does not make sense):

I am guessing that Mr Eaqub also aggregates all property as a giant average, in making the sweeping statement that 'owning a house is bad business'. If he said 'owning a house in a low growth area is bad business', I might agree. But in the context of Auckland, Canterbury and other better capital growth areas, I think his advice reveals yet another economist talking in averages that are not reflective of regional variances in capital growth rates.

Moreover, many economists who provide commentary on property make the assumption that the population is average, they invest in averages and get the average outcome. This is overly simplistic, because it assumes you are not smart enough to do the maths and work out where you can get above average capital growth in property. For example, a home owner can beat the market average by buying subdivisible property (e.g. buy something that is being rezoned under the Auckland Unitary Plan to get better growth rates – I have been buying heaps of these properties for my own portfolio because it is obvious these assets will jump in value when the new zoning rules come in). In summary, dealing in averages ignores your ability to add value to the returns gained through home ownership by being intelligent in your choice of property and picking the better assets.

So I say:

Let’s look at a second argument that arises from Mr Eaqub’s property bashing stance. He has said that you are better to sell your home and invest your equity in the stock market. This pre-supposes that the stock market beats property investment. More particularly, property investment is normally leveraged, so he presupposes that the stock market beats leveraged property investment.

In short, I wonder why Mr Eaqub does not suggest instead as a more balanced view to ‘sell your home if it is in a low growth area, and buy a mix of leveraged property investment in high growth areas and some shares’. This would result in a more diversified return and provide the benefit of leveraged high growth property assets for part of the return. Most authorised financial advisers I have met take this approach when advising my firm’s clients in financial planning engagements.

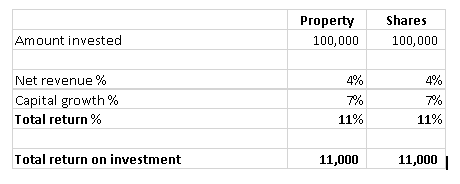

Take the following example showing identical returns between property and shares as a hypothetical analysis. Recall that to compare two investments, you should be thinking about the total return derived from the different asset classes (i.e. the after tax cash flow added to the capital growth).

For argument’s sake, let’s look at these and assume a similar rate of return, given that the markets are perfectly competitive and over time the returns should be similar. (Economic theory would say capital will chase higher returns and compete away any supernormal profits to equalise/normalise returns over time.)

Unleveraged investment, hypothetical identical return assumption

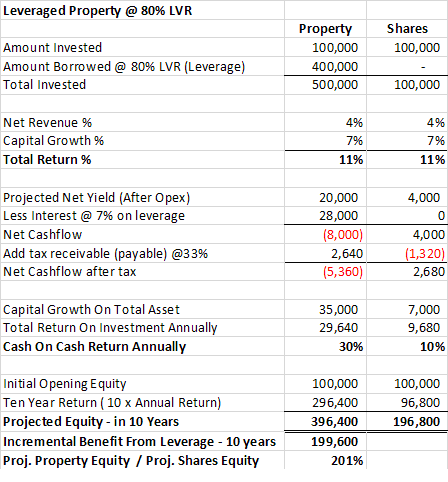

But people generally use 80% leverage in their residential property investment. Now let’s look at the returns with the costs of leverage and benefit of capital growth factored in.

As you can see, investing the same amount ($100,000) on identical returns (which I have made up for argument’s sake), provides a very different result with leverage applied to property. Property wins hands down.

Of course for devil’s advocate, we might say you can leverage shares. I would reply firstly that this is much riskier due to the propensity to have a rapid market movement in the stock market and margin call by a bank (on the leveraged shortfall). Secondly, leverage offered by New Zealand bankers tends to be limited to 50% on lower risk shares, reducing leverage and restricting yield to that derived from blue chip stock. Thirdly, you end up with interest/cash flow issues on most stocks (as many will not pay a dividend and instead retain earnings), making the investment extremely cash flow negative if you leverage it (until you sell). I hope that makes sense.

Right throughout the GFC I encouraged clients to focus property investment in the Auckland property market (and I continue to do so). The yield averages cited by various commentators (on Auckland yields) assume the investor is uninformed and buying on averages. I don’t know many investors who are this uninformed to be frank – it seems the investors know more about the topic that the commentators here.

Parochial investors in small towns are less likely to be rewarded in the long run with good growth. With the exception of Canterbury and maybe Hamilton and Wellington, the smaller cities and provinces just don’t have the fundamentals that support a commanding capital growth story in my view. I prefer areas with tight supply, sustainable demand and high incomes to support a growth environment. Call me a Jafa, but the winner will always be Auckland in a capital growth contest in NZ.

Summary

I therefore conclude owning your home is a good business to be in.

Past performance is not a guarantee of future performance. This article is generic discussion and should not be construed as financial advice.

Hi Salesh, I just wanted to send you an email on behalf of GRA to say how fantastic we have found your company to date. As you know, Ben and I joined GRA a couple of months ago and have just found you so amazingly helpful in getting our new property set up correctly and sorted out. We have what I would consider a rather complicated structure as a result and it’s a fantastic feeling to know that we are getting everything done in the best way possible. We have just had approval to put a minor dwelling on the property which will make a massive difference in terms of cash flow and obviously value, something we would never have even thought of without GRA and which we are very excited about. During the buying process we attended a seminar with Matthew and from the outset thought he was fab. We therein signed up for property school and found this nothing short of fantastic. The content was relevant, up to date and comprehensive, but more importantly it was taught in a way that we could actually understand and really get value out of. I wanted to mention also, that everybody GRA have recommended to us has been just so efficient and absolute masters at what they do. A wonderful network of people that we feel very lucky to now be able to call on. From Kris Pederson and Bryan Rist who put our mortgage together to the insurance guys they then referred us to, I’m super impressed. Within GRA, Ellery has probably turned things around for us faster than I’ve ever known before, something which we appreciated so very much when it came to crunch time. She’s always a pleasure to deal with and again, we’re stoked. We’ve just settled on the property today and are about to go and get the keys. I’m pretty pumped and hence this email is probably rather excitable. So, a massive thank you to you Salesh, the partners for such a fabulous 6 weeks at property school and everyone at GRA for their help. May this be the start of our property empire. Thanks again, - A & B - July 2015

Investing in residential property?

If you're investing in residential property, seeking to maximise your ability to succeed and minimise risk, then this is a 'must read'.

Matthew Gilligan provides a fresh look at residential property investment from an experienced investor’s viewpoint. Written in easy to understand language and including many case studies, Matthew explains the ins and outs of successful property investment.